Your brilliant hardware product is irrelevant if your unit economics don’t align with the venture capital model.

- Hardware’s capital-intensive nature—inventory, tooling, logistics—creates a burn rate and risk profile that is fundamentally misaligned with the fast-scaling, high-margin expectations of SaaS-focused VCs.

- Market validation from crowdfunding is not business validation for VCs, who see it as a measure of desire, not a repeatable and scalable revenue engine.

Recommendation: Stop pitching your product’s features and start defending its financial model. Master your Bill of Materials (BOM), capital physics, and margin erosion to speak the language investors understand.

You’ve poured everything into your prototype. It’s sleek, functional, and solves a real problem. You draft the perfect pitch deck, line up meetings, and then comes the email. It’s polite, but the message is brutally clear: “Fascinating product, but we’re passing. It’s hardware.” You’re told “hardware is hard,” that it requires too much capital, or that it isn’t scalable like software. These are the common refrains, the platitudes that serve as a convenient shorthand for a much harsher reality.

The frustration is understandable. Founders believe a great product should be enough. They see a successful Kickstarter campaign as undeniable proof of market fit. But from the other side of the table—the venture capitalist’s side—these signals mean something entirely different. The core issue isn’t that your product is bad or that the market doesn’t want it. The issue is that the very nature of building and selling physical objects breaks the financial and risk models that have made VCs wealthy in the world of software.

The truth is, your startup’s failure or success in fundraising has less to do with your product vision and more to do with your grasp of capital physics. Atoms are more expensive to move than bits. This isn’t just a challenge; it’s a different game with different rules. Instead of focusing on why hardware is difficult, we must dissect *why* it is so often un-investable from a traditional VC perspective. This requires moving beyond product features and into the unforgiving world of inventory cash cycles, compliance costs, margin erosion, and factory audits.

This article will not offer you sympathy. It will provide the unflinching financial breakdown that most VCs won’t give you. We will dissect the critical financial hurdles that kill hardware startups and equip you with the strategic framework to build a business that is not just innovative, but investable.

This guide provides a direct look into the financial realities and operational hurdles that define hardware ventures. By understanding these core challenges from an investor’s perspective, you can better navigate the path from prototype to production and, ultimately, to a fundable company.

Summary: The Unforgiving Economics of Hardware Startups

- Why You Need 3x More Capital Than You Think for Inventory?

- How to Plan for Compliance Testing Without Delaying Launch?

- Kickstarter or Seed Round: Which Validates Hardware Better?

- The “Free Shipping” Error That Bankrupts Hardware Campaigns

- How to Reduce Your BOM Cost by 15% Without Sacrificing Quality?

- Why High Burn Rates Kill More Startups Than Lack of Product Vision?

- How to Audit a Factory for Quality Control remotely?

- How Rapid Prototyping With 3D Printing Cuts Development Costs by 50%?

Why You Need 3x More Capital Than You Think for Inventory?

The single most common point of failure for a hardware startup isn’t the product; it’s the cash flow gap created by inventory. Unlike a SaaS company that can sell and deliver its product instantly, you must pay for components and manufacturing long before you see a single dollar of revenue. This isn’t a minor detail; it’s the central problem of hardware’s capital physics. Founders consistently underestimate this need, budgeting for one production run when they should be planning for three distinct pools of inventory: raw materials, work-in-progress (WIP), and finished goods.

The cycle is brutal. You pay your supplier upfront. Manufacturing takes 8-12 weeks. Shipping and customs add another month. Only then can you begin to sell and collect revenue. This means your capital is frozen for months. To survive, you don’t just need cash for one cycle; you need enough working capital to fund the second production run while the first is still in transit or sitting in a warehouse. This is the hardware “valley of death.” In fact, MIT research shows hardware startups need enough cash to cover 3-6 months of operating expenses just for working capital, a figure that shocks most first-time founders.

This financial drag is compounded by hidden costs. A firmware bug discovered post-production can render thousands of units unsellable. A customs hold can delay revenue for weeks, while storage fees continue to accrue. And then there are returns and RMAs (Return Merchandise Authorizations), which require even more capital to refurbish or dispose of defective units. Without a deep, multi-cycle cash reserve, even a startup with strong pre-orders is just one supply chain hiccup away from insolvency.

Your financial model must account for these brutal realities. A spreadsheet that ignores supplier payment terms, production cycle times, and potential inventory write-offs is not a plan; it’s a fantasy. And VCs do not invest in fantasies.

How to Plan for Compliance Testing Without Delaying Launch?

If inventory is the financial black hole, compliance testing is the black hole for your timeline. Founders often treat certifications like FCC (for the U.S.) and CE (for Europe) as a final checkbox before launch. This is a catastrophic mistake. Compliance is not a step; it is an integrated part of the design process, and failing to plan for it from day one introduces massive, un-quantified risk that investors will spot immediately.

Pre-compliance testing should happen early and often. Using a certified lab to test your early prototypes can identify radio frequency (RF) emission failures or safety issues while the cost of fixing them is still low. A design change on a PCB is cheap; a change to a hardened steel injection mold tool is not. The cost of re-tooling can run into tens or hundreds of thousands of dollars, not to mention the weeks or months of delay. One expert recounts a harrowing tale of a company that performed 17 trial runs on a plastic tool before it was accepted, with each run taking at least a week. That’s over four months of delay for a single component, a death sentence for a cash-strapped startup.

Choosing your target markets dictates your compliance path and associated costs. A product sold in both the US and EU requires navigating two different, albeit overlapping, regulatory landscapes. Founders must see this not as a burden, but as a strategic decision with significant budget and timeline implications.

This table outlines the high-level strategic differences between FCC and CE certifications, information critical for budgeting and go-to-market planning.

| Aspect | FCC (US) | CE (Europe) |

|---|---|---|

| Primary Market | United States | European Union |

| Typical Costs | Part of fixed costs per design | Similar certification requirements |

| Testing Complexity | Focus on radio/bluetooth emissions | Broader safety requirements |

| Time to Completion | 4-8 weeks typical | 6-12 weeks typical |

| Strategic Value | Essential for US market entry | Opens 27-country market |

An investor sees a line item for “Certification” in a budget and immediately probes. Have you done pre-compliance? Have you budgeted for failures and re-testing? If your answer is vague, the meeting is over. You haven’t de-risked the launch; you’ve merely hidden the risk from yourself.

Kickstarter or Seed Round: Which Validates Hardware Better?

Founders love to present a successful Kickstarter campaign as the ultimate validation. “We raised $1 million from 10,000 backers! We have product-market fit!” From a VC’s perspective, this is a dangerous misconception. Crowdfunding validates market *desire*, not a scalable, profitable *business*. It proves that people want your product, but it says nothing about your ability to manufacture it at scale, deliver it on time, or build a company with healthy unit economics. This is the classic validation mismatch.

A one-time “hardware hit” can be a fantastic outcome for an entrepreneur, but it doesn’t align with the venture capital model, which is built on repeatable, high-growth revenue streams. As one industry analysis bluntly puts it:

There is nothing wrong with a one-time hardware hit. I’ve read of entrepreneurs who’ve had one product sell to hundreds of thousands of people and the entrepreneur rides off into the sunset. While that works for the entrepreneur and their family, it doesn’t work for VC.

– Hardware Industry Analysis, HackerNoon

The intelligent approach is a hybrid strategy. Use crowdfunding as a tool for initial validation and to generate non-dilutive cash for your first tooling and production run. But the real work begins after the campaign ends. You must leverage the campaign’s momentum and metrics—customer acquisition cost, geographic demand, attachment rates for accessories—as proof points in your pitch to seed investors. The crowdfunding success becomes a de-risking event, demonstrating that a core market exists. You then raise a seed round not to *build* the product, but to *scale* the business: building a team, optimizing the supply chain, and establishing distribution channels.

Pitching a Kickstarter success as the end of the story is naive. Pitching it as the first chapter—a data-rich prologue to a scalable business—is how you get a VC to lean in and listen.

The “Free Shipping” Error That Bankrupts Hardware Campaigns

Nothing reveals a founder’s inexperience faster than their shipping and logistics plan. Offering “free worldwide shipping” on a Kickstarter campaign is a rookie error that signals an immediate lack of financial discipline. Logistics are not a marketing expense; they are a core component of your Cost of Goods Sold (COGS), and every miscalculation directly erodes your already thin hardware margins. This is where margin erosion becomes a terminal disease.

The cost of shipping a physical product is far more than the postage fee. It’s a complex stack of expenses that can easily dismantle a business plan. You must account for:

- Packaging: Custom boxes, protective inserts, and branding all have a per-unit cost.

- Warehousing & Fulfillment (3PL): Storing products and paying a third-party logistics provider to pick, pack, and ship orders.

- International Duties & Taxes: These vary wildly by country and can add 20% or more to the product’s cost, often unexpectedly billed to the customer, creating a support nightmare.

- Returns & Reverse Logistics: The cost to receive, inspect, and restock or dispose of returned items is significant.

- Scrap & Damage: A percentage of units will be damaged in transit, and you must bear that cost.

These aren’t edge cases; they are guaranteed costs. As one analysis of hardware startups notes, seemingly small complications in this area quickly cascade into existential threats. Research shows that shipping-related costs including duties and returns must be calculated meticulously as a percentage of your Bill of Materials (BOM) cost. Ignoring them means your gross margin is a work of fiction. A hardware business lives and dies by its gross margin. If you can’t demonstrate a clear, defensible path to a 50%+ margin after all logistics costs, you don’t have a venture-scale business.

Expert Observation: The Cash Flow Trap

Industry experts consistently warn that regardless of the initial capital raised, hardware startups are uniquely vulnerable to a cash flow trap. Rising upfront costs, combined with unfavorable manufacturing contracts and unforeseen shipping complications, inevitably lead to major disruptions in both cash reserves and delivery timelines, creating a perfect storm for failure.

When an investor sees “free shipping,” they don’t see a generous offer. They see a founder who hasn’t done the math and a business that’s already on a path to bankruptcy.

How to Reduce Your BOM Cost by 15% Without Sacrificing Quality?

Your Bill of Materials (BOM) is the DNA of your product’s financial health. While founders obsess over the retail price, VCs obsess over the BOM cost. Every dollar saved on the BOM is a dollar that flows directly to gross margin, which in turn fuels growth, marketing, and future R&D. A high BOM cost is a permanent anchor on your company’s potential. The good news is that a 15% reduction is often achievable without compromising quality, but it requires strategic discipline, not just last-minute haggling.

The most effective cost-down strategies are implemented during the design phase. Engaging in Design for Manufacturing (DFM) with your contract manufacturer (CM) is non-negotiable. They can identify components that are expensive, hard to source, or require complex assembly steps. Another powerful tactic is component standardization. Instead of using five different types of screws, design the product to use one. This allows for bulk purchasing and simplifies the assembly line. In fact, KINGBROTHER’s engineering data shows that a 15-20% cost reduction can be achieved through strategic component standardization alone.

Furthermore, you must fight the urge to specify only brand-name components. Your CM often has high-volume purchasing agreements for generic or alternative parts that are functionally identical but can be 30% cheaper. Designing your PCB to accept multiple pre-approved alternative components for key parts (like resistors or capacitors) gives you immense negotiation leverage and protects you from single-supplier stockouts. A smart founder partners with a CM not just for their assembly line, but for their purchasing power.

Action Plan: Slashing Your BOM Costs

- Request a Free BOM Analysis: Ask your Contract Manufacturer (CM) for a cost-reduction analysis. This is often a free service they provide to win your business and demonstrates their value as a partner.

- Implement DFM Principles Early: Integrate Design for Manufacturing (DFM) feedback from your CM at the earliest stages of the design process to avoid costly re-engineering later.

- Cross-Reference Components: Actively search for generic or alternative components that meet your specifications. Cross-referencing brand-name parts can unlock savings of up to 30%.

- Consolidate and Standardize: Use the same components across multiple product lines or within a single product wherever possible to increase order volumes and unlock volume purchasing discounts.

- Leverage Your CM’s Volume: Partner with a CM based on their existing high-volume purchases of common components, piggybacking on their established supply chain and pricing power.

A founder who can articulate a clear BOM cost-down strategy is demonstrating a sophisticated understanding of unit economics. You’re not just a product visionary; you’re a business operator. That’s who gets funded.

Why High Burn Rates Kill More Startups Than Lack of Product Vision?

In the SaaS world, high burn rates are often a sign of aggressive growth—hiring sales teams and pouring money into marketing to acquire customers with a high lifetime value. In hardware, a high burn rate is a wildfire consuming a finite pile of cash with no guarantee of recurring revenue on the other side. This fundamental difference in capital efficiency is why VCs view hardware and software through entirely different lenses. Your product vision is irrelevant if you run out of money before you can ship.

Compared to software, hardware is more challenging to meet market needs, has more unpredictable manufacturing risks, has more complicated sales and distribution processes, and generally requires more time to scale. VCs that expect to exit early have no incentive to invest in risky hardware startups.

– Monozukuri Ventures, Why VCs Avoid Hardware Startups

The SaaS model is beautiful in its simplicity: for every dollar spent on sales, a company might see a dollar of annual recurring revenue (ARR) in less than a year. This leads to high valuation multiples, often 10 to 20 times revenue. Hardware doesn’t work that way. A dollar spent today goes to inventory that might not generate a one-time sale for six months, with margins that are a fraction of software’s. The time to scale is longer, the risks are higher, and the capital required is immense. This is the risk stack of hardware: layers of manufacturing, supply chain, and logistics risk that simply don’t exist in software.

The following table starkly illustrates why the venture capital model is structurally biased towards SaaS. The metrics that VCs live by—capital efficiency, revenue models, and valuation multiples—all favor the predictable, scalable nature of software over the capital-intensive reality of hardware.

| Factor | Hardware Startups | SaaS Startups |

|---|---|---|

| Capital Efficiency | Lower – requires manufacturing, inventory | Higher – SaaS companies can be highly capital efficient |

| Revenue Model | One-time sales, challenging margins | For every dollar spent on sales, can see a dollar of recurring revenue in less than a year |

| Valuation Multiples | Lower due to capital intensity | Often valued at 10 to 20 times annual revenue |

| Time to Scale | Longer due to production cycles | Rapid with cloud distribution |

| VC Investment 2022 | Significantly less than software | $62.4 billion in enterprise SaaS in 2022 |

Your job as a founder is not to pretend you’re a SaaS company. It’s to demonstrate that you have an iron grip on your burn rate, a realistic plan for your cash runway, and a clear path to profitability that acknowledges the unforgiving realities of the hardware business model.

How to Audit a Factory for Quality Control remotely?

In a post-pandemic world, the inability to jump on a plane and walk a factory floor is no longer an excuse for poor quality control. A founder who claims they need to be “on the ground” to ensure quality is revealing a lack of process. Robust, remote QC is not only possible, it’s a sign of an operationally mature startup. An investor needs to see a system, not a dependency on one person’s travel schedule.

The cornerstone of remote QC is trust, but verify. You start by hiring a professional third-party inspection service based in the same region as your factory. They are your eyes and ears on the ground. However, they are useless without an exceptionally clear set of instructions from you. This includes sending them a “Golden Sample”—a perfect, approved unit that serves as the benchmark for all production. You must also provide “Limit Boards,” which are physical examples showing the absolute boundaries of acceptable cosmetic defects (e.g., “this level of scratch is okay, this level is not”).

Case Study: A Structured Remote Manufacturing Plan

A successful remote QC strategy requires a mature product manufacturing plan well before volume production begins. This involves finalizing all documentation, defining a clear bill of materials (BOM) structure, and establishing a product cost model with the finance team. A critical component is the product-test plan, which includes working with vendors to build and validate custom test fixtures for the assembly line. Furthermore, proactive discussions with contract manufacturing partners about a future cost-reduction program should be initiated early, building a framework for long-term quality and efficiency.

Data and evidence are your weapons. Demand daily production yield reports from your factory, showing the number of units passed versus failed at each QC station on the line. A sudden drop in the yield rate is your earliest warning sign of a problem. Don’t rely on photos; demand specific, unedited video evidence. Request footage of new component batches being unboxed, random clips of the assembly line in action, and demonstrations of QC technicians performing specific tests. If you can’t see it, it didn’t happen.

When an investor asks how you manage quality, “I have a great relationship with the factory owner” is the wrong answer. The right answer is a detailed walkthrough of your remote inspection briefs, your yield rate monitoring, and your evidence-based verification process. You’re not managing a relationship; you’re managing a system.

Key Takeaways

- Capital Physics is King: Hardware’s need for upfront capital for inventory and tooling creates a cash flow “valley of death” that is fundamentally at odds with the capital-efficient SaaS model VCs prefer.

- Margins are Non-Negotiable: Unlike software’s near-zero marginal costs, every physical unit has a cost (BOM, logistics, duties, returns) that relentlessly erodes margins. A clear path to 50%+ gross margin is essential.

- Risk is Stacked: Hardware carries a “risk stack”—manufacturing, supply chain, compliance, logistics—that doesn’t exist in software. VCs price this risk into their valuation, if they invest at all.

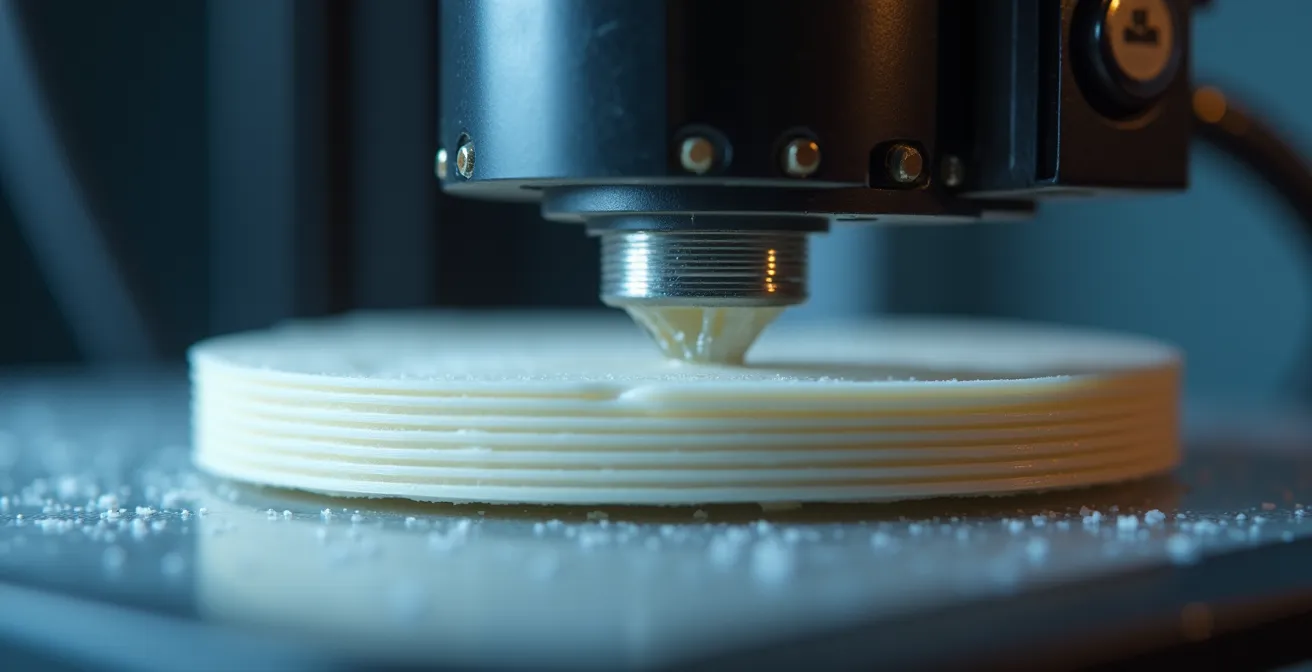

How Rapid Prototyping With 3D Printing Cuts Development Costs by 50%?

The journey from idea to a manufacturable product is long and expensive. Historically, each iteration of a physical prototype required custom tooling and weeks of waiting, burning through cash and time. Today, rapid prototyping, particularly with 3D printing, has fundamentally changed this equation. A founder who isn’t leveraging this technology is willfully ignoring one of the most powerful de-risking tools available and signaling to investors that they are wasting capital.

The strategic value of 3D printing isn’t just about speed; it’s about the cost of learning. Every prototype is a learning cycle. It allows you to test ergonomics, check mechanical fit, and get tangible user feedback while changes are still just a modification to a CAD file. Finding out a button is in the wrong place via a $50 3D print is a minor adjustment. Finding out after you’ve spent $50,000 on an injection mold is a disaster. As one real-world example illustrates, a team can spend nine months just talking to users and building prototypes to get a product ready for manufacturing. Compressing these iteration cycles is a direct saving of your most precious resource: cash runway.

This process directly impacts your bottom line. By iterating quickly and cheaply, you can finalize your design with greater confidence, reducing the risk of costly changes to hard tooling. This directly translates to a lower overall development cost and a faster path to revenue. The ability to produce multiple design variations in a single day allows for parallel experimentation that was previously unthinkable. Case studies in related engineering fields have shown that this kind of optimization can deliver massive savings, in some instances up to $2.4M per year through better design and material choices discovered during prototyping.

For an investor, a detailed rapid prototyping strategy is evidence of capital efficiency. It shows you respect the cost of time and have a plan to learn faster and cheaper than your competition. It proves you understand that in the world of hardware, the best way to save money tomorrow is to spend a little on learning today.